Many Not-For-Profit and Charitable organizations struggle with understanding the difference between the deferral and restricted fund methods of recognizing contributions. RLB’s Not-For-Profit team presented on this topic at their December 2020 Coffee Talk webinar presented by Colleen Gallagher and Michelle Steele.

The following goes into detail on both the deferral and restricted fund methods and provides guidance on how to record the three types of contribution under each method.

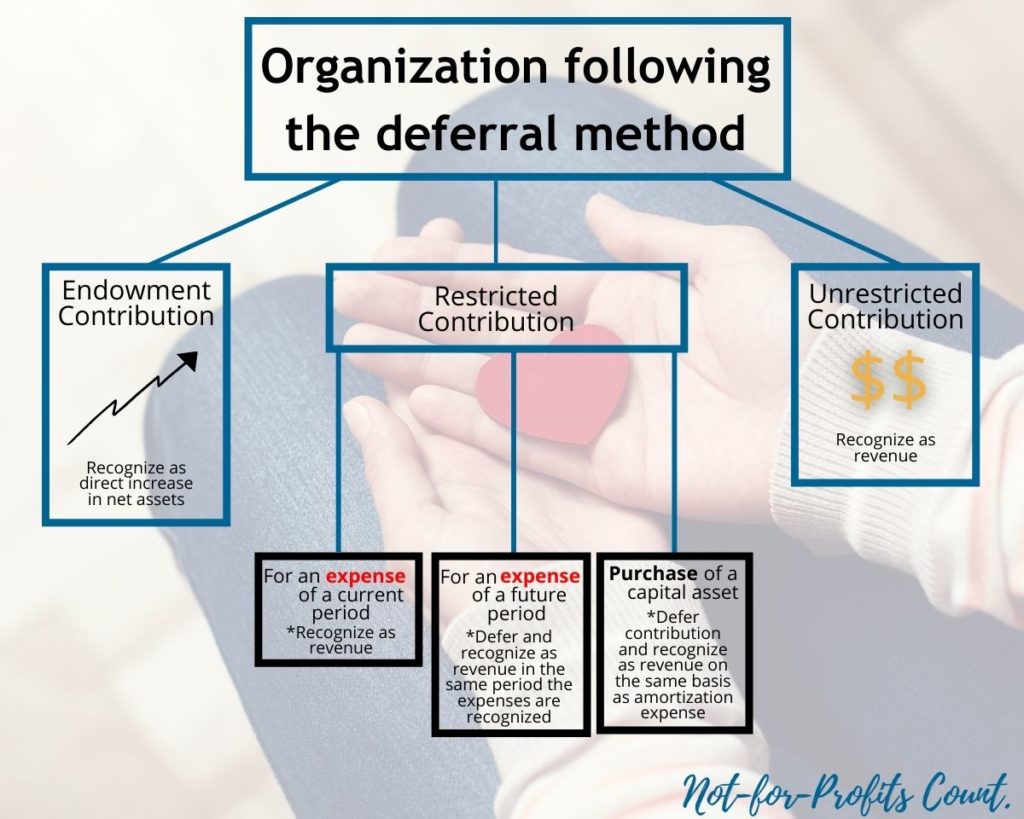

Deferral Method

The purpose of the deferral method is to match the contributions received with the related expense so there is less volatility in the net operating surplus as revenue is recognized in the same period as the expense.

With the deferral method, you typically have one fund – The General Operating Fund (which is unrestricted). However, you can choose to create multiple internally restricted funds within net assets. Therefore, you would have the General Operating Fund AND Internally restricted funds (which are funds set aside within net assets at the board’s discretion). Interfund transfers would be recorded from the General Operating Fund to any internally restricted funds (or vice versa).

The following charts summarize the flow of how the various contributions are recognized using the deferral method:

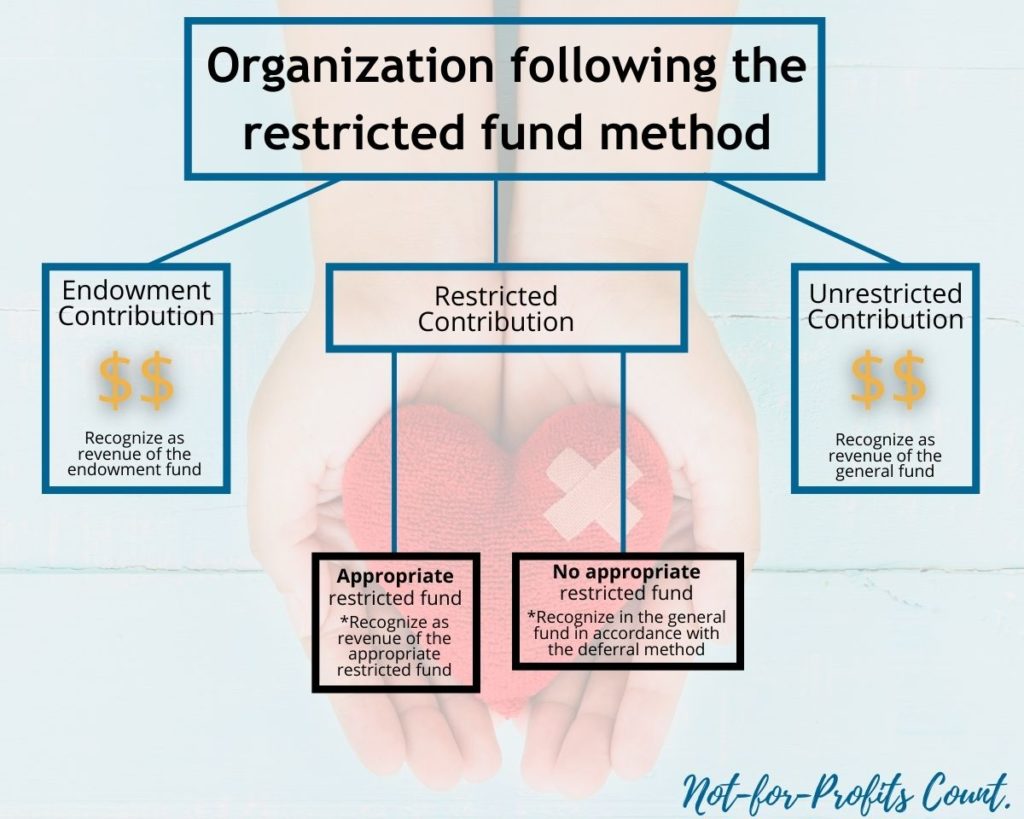

Restricted Fund Method

The specialized use of fund accounting, where each restricted fund is a self-balancing set of accounts – the activities for each fund can be accounted for separately.

There is more volatility in the net surplus with this method as revenue is recognized immediately within each fund (compared to the deferral method where the purpose is to match revenue with the related expense). However, each restricted fund net asset balance clearly distinguishes the total of funds available to be expended on the restricted activity. This provides a better measure of the surplus or deficiency in the restricted fund.

The following charts summarize the flow of how the various contributions are recognized using the restricted fund method:

Recording Contributions under each method

Contributions are the non-reciprocal transfer to a charity or not-for-profit organization of cash or other assets or a non-reciprocal settlement of the cancellation of its liabilities.

There are 3 types of Contributions:

- Externally Restricted – a contribution subject to externally imposed stipulations that specify the purpose for which the contributed cash or other asset is to be used (ie. a contribution restricted for a specific program or the purchase of a capital asset)

- Endowment – a restricted contribution subject to externally imposed stipulations specifying that the resource contributed be maintained permanently.

- Unrestricted – a contribution that is neither restricted nor an endowment.

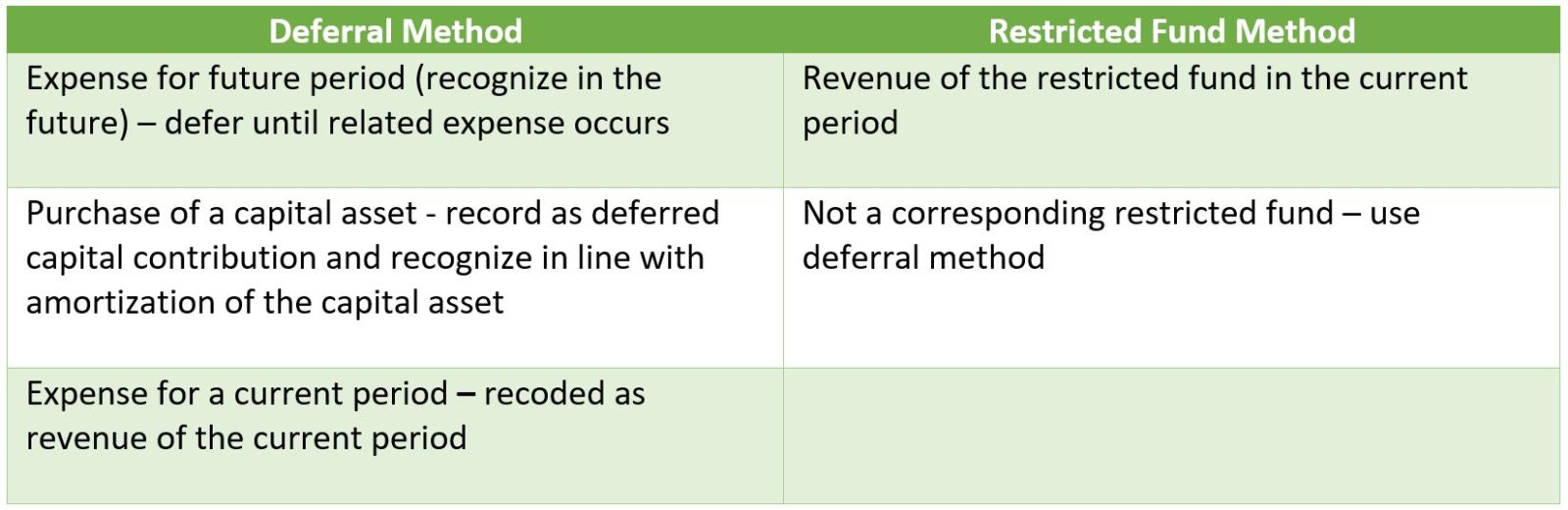

The deferral and restricted fund methods are compared below for each of the 3 types of contribution:

1) How to record Contributions – Externally Restricted:

Externally Restricted: a contribution subject to externally imposed stipulations that specify the purpose for which the contributed asset is to be used.

2) How to record Contributions – Endowment:

Endowment: a restricted contribution subject to externally imposed stipulations specifying that the resource contributed be maintained permanently.

3) How to record Contributions – Unrestricted:

Unrestricted: a contribution that is neither a restricted nor an endowment.

Not-For-Profit and Charitable organizations can also have revenue in addition to contributions.

Revenue is the inflow of cash, receivables or other consideration arising in the course of ordinary activities, which is normally from the sale of goods, the rendering of services and the use by others of resources (ie. interest and dividends).

Revenue can be recognized when the requirements of performance are satisfied, and collection is reasonably assured. Performance would be achieved when the following is met:

- The seller has transferred to the buyer the significant risk and rewards of ownership (ie. evidence of an arrangement exists, delivery of goods, seller’s price is fixed)

- Reasonable assurance exists regarding the measurement of the consideration

Some examples of revenue are membership fees, sale of goods and services, program fees, and investment revenue.

The deferral and restricted fund methods are compared below for the recognition of revenue:

Our Not-For-Profit team specializes in charities and not-for-profit organizations, please reach out to Colleen Gallagher or Michelle Steele with any questions.

Read Part 2 of this blog “Reserves and Fund Balances” today.