In Part 1 we reviewed the 3 types of contributions and how each is recognized using both the deferral method and restricted fund method. Here we discuss the net asset treatment under both the deferral method and restricted fund method. RLB’s Not-For-Profit team presented on this topic along with Contributions at their December 2020 Coffee Talk webinar presented by Colleen Gallagher or Michelle Steele.

Net Assets

Are an accumulation of prior years’ net surplus (deficits) that are reinvested in the organization. These are often referred to as fund balances or reserves.

Net assets may be internally or externally restricted:

- Externally restricted net assets have stipulations imposed from outside the organization that specify how the resources must be used. An example would be a fund for a future building.

- Endowments are restricted contributions subject to externally imposed stipulations specifying that the resource contributed be maintained permanently.

- Internally restricted net assets are funds set aside at the board’s discretion. An example would be a contingency fund.

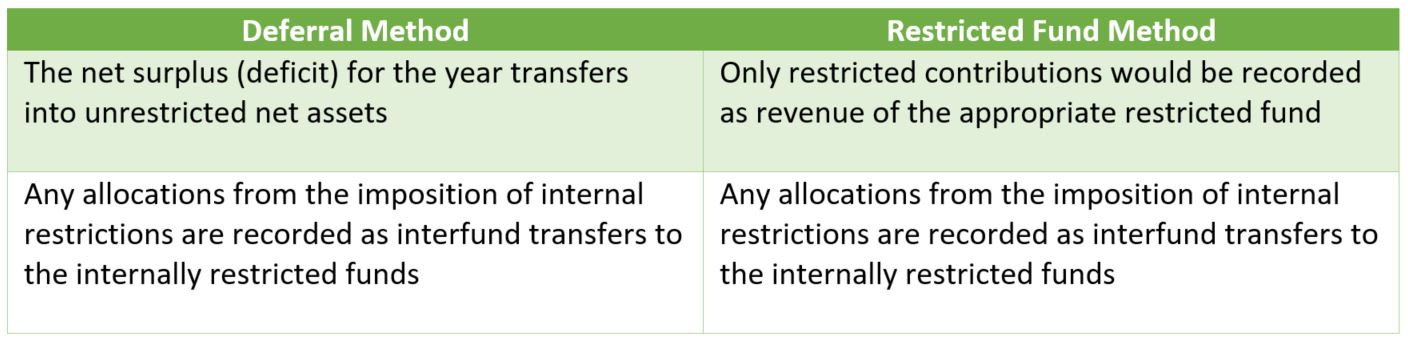

These types of net asset are summarized below for each of the deferral and restricted fund methods:

1) Externally Restricted:

Externally restricted fund balances have stipulations imposed from outside the organization that specify how the resources must be used (ie. for specific expenses, grant received for capital assets).

2) Endowment:

Endowment: a restricted contribution subject to externally imposed stipulations specifying that the resource contributed be maintained permanently

3) Unrestricted:

Our Not-For-Profit team specializes in charities and not-for-profit organizations, please reach out to Colleen Gallagher or Michelle Steele with any questions.